How the CFD Business Model Really Works Behind the Scenes

The retail trading landscape has undergone a dramatic transformation over the past decade. According to market research from Market Reports World, the global CFD broker market was valued at approximately $2.53 billion in 2025, with projections indicating growth to $4.04 billion by 2033. Behind these figures lies a sophisticated operational framework that most traders never see: the CFD business model that powers modern brokerage operations.

For aspiring brokerage owners, existing brokers looking to optimize operations, or institutional players considering entry into the retail CFD space, understanding the mechanics of trade execution, risk management, and revenue generation is essential. Comprehending these elements determines the difference between sustainable profitability and operational failure. The CFD business model operates on principles fundamentally different from traditional asset ownership, creating unique operational dynamics that require specialized infrastructure to manage effectively.

Trade Execution Flow in CFD Brokerages

When a retail trader clicks “buy” on a CFD platform, a complex sequence of technological and financial processes initiates within milliseconds. The broker’s technology stack immediately performs several critical validations: account authentication, available margin verification, instrument availability checks, and compliance screening. Modern CFD platforms process these checks in under 50 milliseconds.

Once validated, the order enters the broker’s decision tree. This sophisticated algorithm determines routing based on trade size, client classification, current market volatility, and the broker’s real-time risk exposure. This routing logic represents the operational heart of the CFD business model, where commercial strategy meets technological execution.

For brokers operating with a White Label Solution For CFD Brokerage, this entire infrastructure, from order routing to risk management systems, comes pre-configured and battle-tested. Leverate’s all-in-one platform handles the complete trade lifecycle, allowing new brokers to focus on client acquisition rather than building complex execution technology from scratch.

The execution layer integrates multiple components simultaneously: the pricing engine pulls real-time quotes from liquidity providers, the risk management system calculates position impact on overall exposure, and the transaction processor prepares settlement instructions. Advanced CFD platforms also implement intelligent order matching. If opposing client orders arrive simultaneously, sophisticated brokers can internally match these positions, reducing external hedging costs while maintaining identical execution quality.

A-Book and B-Book Exposure Management

The terminology “A-Book” and “B-Book” represents one of the most misunderstood aspects of the CFD business model. These aren’t merely technical labels; they describe fundamentally different approaches to managing market risk that directly impact broker profitability.

A-Book execution routes client trades directly to external liquidity providers. When a trader opens a position, the broker immediately mirrors that exact trade with a prime broker or liquidity pool. The broker earns revenue through spread markup or commission, but assumes no market risk from price movements. This model offers complete transparency and eliminates conflicts of interest, though it requires substantial operational infrastructure and established relationships with tier-1 liquidity providers.

B-Book execution takes the opposite approach. The broker acts as the counterparty to client trades, internalizing positions within their own book. When a client loses money, in some cases, the broker can profit from that loss. Conversely, client profits represent direct broker losses. However, B-Book operations aren’t inherently problematic when managed professionally. The model allows brokers to offer fixed spreads, instant execution even during low liquidity periods, and lower minimum deposits that attract retail participants.

The reality is that most successful CFD brokers operate hybrid models, sometimes called C-Book execution. Advanced platforms like Leverate’s premium trading platform, along with our plug-and-play solutions, enable dynamic routing logic that automatically allocates trades based on real-time assessment. High-frequency traders and consistently profitable clients route to A-Book execution, while smaller retail traders with predictable patterns remain on B-Book. According to industry analysis, leading brokers internalize between 60-90% of forex flow, demonstrating that professional B-Book operations represent standard industry practice.

Risk Aggregation Across Client Positions

Individual trades represent discrete events, but CFD brokers manage thousands or millions of positions simultaneously. Risk aggregation, the process of calculating net exposure across all client positions, forms the operational backbone of sustainable brokerage operations.

Consider a simplified scenario: 100 clients hold long EUR/USD positions totalling 50 standard lots, while 80 clients hold short positions totaling 45 standard lots. The broker’s actual market exposure is just 5 lots net long, not 95 lots gross. Professional risk management systems calculate these aggregations in real-time across hundreds of instruments, identifying where the broker faces genuine directional risk requiring hedging.

Modern CFD platforms segment risk across multiple dimensions: instrument type, time horizon, client profitability profiles, and correlation between different asset classes. Leverate’s comprehensive infrastructure includes advanced risk management tools that monitor exposure across all instruments and client segments. Our Broker Portal provides real-time dashboards showing net exposure by currency pair, commodity, index, and cryptocurrency.

Risk aggregation also considers temporal factors. Many retail traders close positions within hours or even minutes, creating temporary exposures that often self-liquidate without requiring external hedging. Brokers analyze historical patterns to determine which position types typically close quickly versus those likely to remain open for days or weeks, adjusting hedging strategies accordingly.

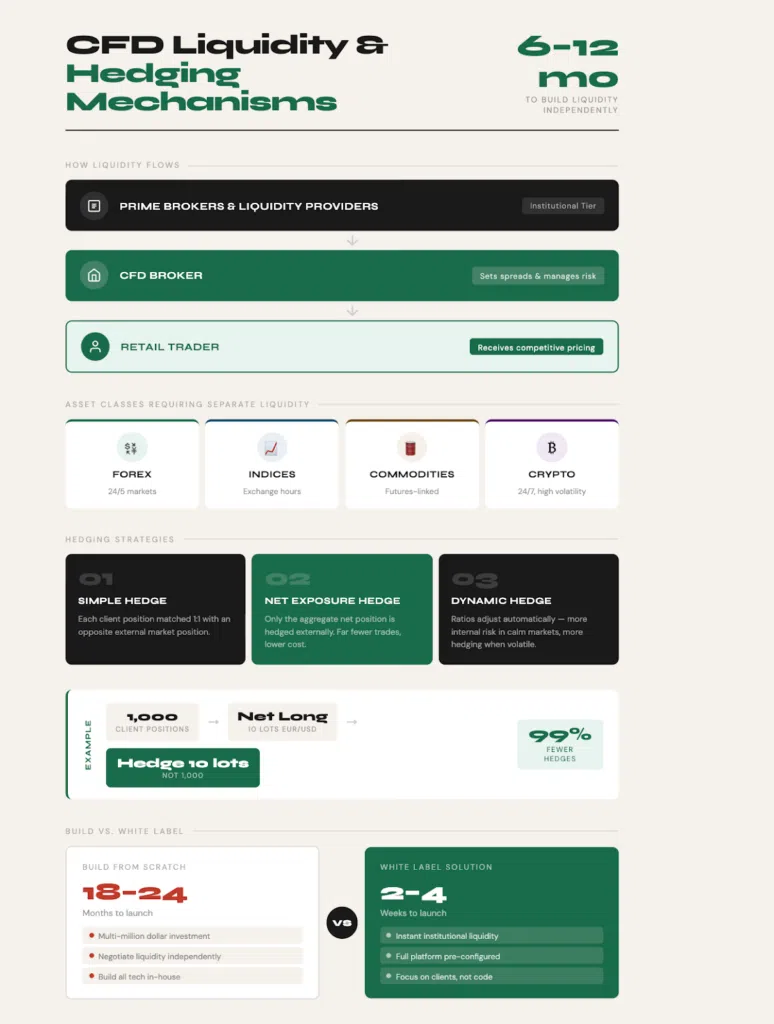

Liquidity Provision and Hedging Mechanisms

Liquidity represents the lifeblood of CFD operations. Without access to deep, reliable liquidity across multiple asset classes, brokers cannot offer competitive spreads or guarantee execution quality during volatile market conditions. Prime brokers and liquidity providers form the external market access layer, determining the raw spreads brokers receive and the competitive pricing they can offer retail clients.

Multi-asset brokers require diversified liquidity across asset classes. Forex liquidity differs structurally from equity index or commodity liquidity. Cryptocurrency CFDs demand specialized liquidity providers equipped to handle 24/7 markets and extreme volatility. Building these relationships independently requires years of institutional networking and substantial capital commitments.

Leverate’s platform includes pre-established liquidity connections across forex, indices, commodities, and cryptocurrencies through Leverate Prime. New brokers gain instant access to institutional-grade pricing without negotiating individual liquidity agreements, a process that typically takes 6-12 months when done independently.

Hedging strategies vary by broker sophistication and risk appetite. Simple hedging involves matching each client position with an equal and opposite position in the external market. More advanced brokers hedge only net exposure, if 1,000 clients collectively hold a net long position of 10 lots EUR/USD, the broker hedges only those 10 lots rather than each position.

Dynamic hedging adjusts based on market conditions. During low volatility with balanced order flow, brokers may warehouse more risk internally. When volatility spikes or positions become imbalanced, automated systems increase hedging ratios to reduce exposure. Some brokers implement time-weighted hedging, where positions held longer than specific thresholds automatically hedge to external markets.

The operational complexity described above explains why most new entrants choose white-label partnerships rather than building infrastructure from scratch. Developing proprietary trading platforms, establishing liquidity relationships, implementing risk management systems, and achieving regulatory compliance requires multi-million dollar investments and 18-24 month development timelines.

Leverate’s solution addresses every component of the CFD business model within a unified ecosystem. Our premium trading platform delivers professional-grade execution with social trading capabilities, TradingView chart integration, and mobile applications. The included CRM system manages the entire client lifecycle from lead acquisition through retention. The Broker Portal provides centralized control over trading conditions, leverage policies, and promotional campaigns, all configurable without development resources.

Implementation timelines demonstrate the efficiency advantage. While building proprietary infrastructure requires 18-24 months, brokers deploying Leverate’s white-label solution can launch fully operational platforms within 2-4 weeks.

Conclusion

The mechanics behind CFD brokerage operations reveal an ecosystem where millisecond execution speeds, sophisticated risk algorithms, and institutional liquidity relationships converge to create potentially profitable trading environments. The distinction between A-Book transparency and B-Book internalization isn’t about ethical superiority; it’s about matching operational models to business objectives and client demographics.

What separates successful brokers from failed ventures is infrastructure sophistication. The CFD business model demands real-time risk aggregation across thousands of positions, dynamic hedging that responds to market volatility, and liquidity depth across multiple asset classes. These aren’t optional enhancements; they’re operational prerequisites in markets where retail participants increasingly employ algorithmic strategies and institutional-grade analysis tools.

The strategic choice facing new market entrants is clear: invest years and millions building proprietary systems, or deploy proven technology that compresses launch timelines from eighteen months to three weeks. As the global CFD market expands into emerging regions, the competitive advantage can go in favor of brokers who can move quickly while maintaining institutional-grade operational standards.

Ready to launch your CFD brokerage with enterprise-grade infrastructure? Leverate’s all-in-one white-label solution provides everything you need to enter the market in weeks, not years. From institutional liquidity through Leverate Prime to the award-winning trading platform, complete CRM, and comprehensive risk management tools, we handle the technology so you can focus on growth. Contact our team today to schedule a personalized demo and discover how we can power your brokerage success.

FAQs

How do CFD brokers actually make their money?

CFD brokers generate revenue through multiple channels depending on their execution model. A-Book brokers earn through spread markups and per-lot commissions, profiting from trading volume regardless of client outcomes. B-Book brokers profit from the spread and net client losses, as they take the opposite side of trades internally. Most successful brokers operate hybrid models that combine both approaches, optimizing revenue while managing risk. Additional revenue sources include overnight financing charges on leveraged positions, inactivity fees, and premium services.

Do CFD brokers trade against their own clients?

The answer depends on the broker’s execution model. B-Book brokers do act as counterparties to client trades, meaning they profit when clients lose and vice versa. However, this isn’t necessarily predatory; professional brokers manage this through risk aggregation and selective hedging rather than manipulating individual client outcomes. A-Book brokers never trade against clients, routing all positions to external liquidity providers. Hybrid brokers dynamically allocate trades based on client profiles, typically sending profitable traders to A-Book execution while managing retail flow internally.

What happens to my trade after I place it on a CFD platform?

Your trade initiates a multi-step process occurring within milliseconds. First, the platform validates your order, confirming account authentication, available margin, and instrument availability. The validated order then enters the broker’s routing logic, which determines whether to execute internally (B-Book), route to external liquidity (A-Book), or use a hybrid approach. Throughout this process, risk management systems continuously calculate exposure, pricing engines update quotes in real-time, and transaction processors prepare settlement instructions. The entire sequence typically completes in under 100 milliseconds.

What is the real difference between A-Book and B-Book?

A-Book brokers operate as pure intermediaries, routing every client trade to external liquidity providers and earning revenue through spreads or commissions. They assume zero market risk from price movements. B-Book brokers internalize client trades, acting as the direct counterparty. They profit from client losses and lose money on client profits. However, B-Book models enable brokers to offer fixed spreads, instant execution during low liquidity, and lower minimum deposits. The operational distinction matters: A-Book requires significant capital for liquidity provider relationships, while B-Book demands sophisticated risk management. Most professional brokers use hybrid models combining both approaches.

How do brokers decide which trades to hedge and which not to?

Brokers employ sophisticated algorithms analyzing multiple factors: client profitability profiles (consistently winning traders typically route to hedged A-Book execution), position size relative to broker capital, trade duration (positions held longer than specific thresholds often hedge automatically), current market volatility levels, and overall exposure concentration. Advanced platforms like Leverate’s Broker Portal provide real-time risk analytics showing net exposure across all instruments. Many brokers set automated hedging thresholdsfor example, hedging any net position exceeding 50 lots in a single currency pair. This dynamic approach allows brokers to optimize their CFD business model based on current conditions rather than following rigid rules.