How Execution Speed Impacts Broker Revenue: Slippage, Latency and Performance

A few milliseconds is not an abstract concept in brokerage operations. It is the difference between a trade filling at the price a client expected and filling at a worse one, a difference that, across thousands of orders per day, accumulates into a meaningful financial and reputational cost. Execution speed impacts broker revenue in ways that are often invisible in standard reporting but reveal themselves in client behaviour, complaint volumes, and the trading patterns of high-value accounts.

Most brokers understand slippage conceptually. Fewer have systematically mapped where in their infrastructure the latency originates, which client segments are most sensitive to it, and what the cost of inaction actually looks like over a quarter. This article examines each of these factors from an operational perspective.

How Does Execution Speed Impact Broker Revenue?

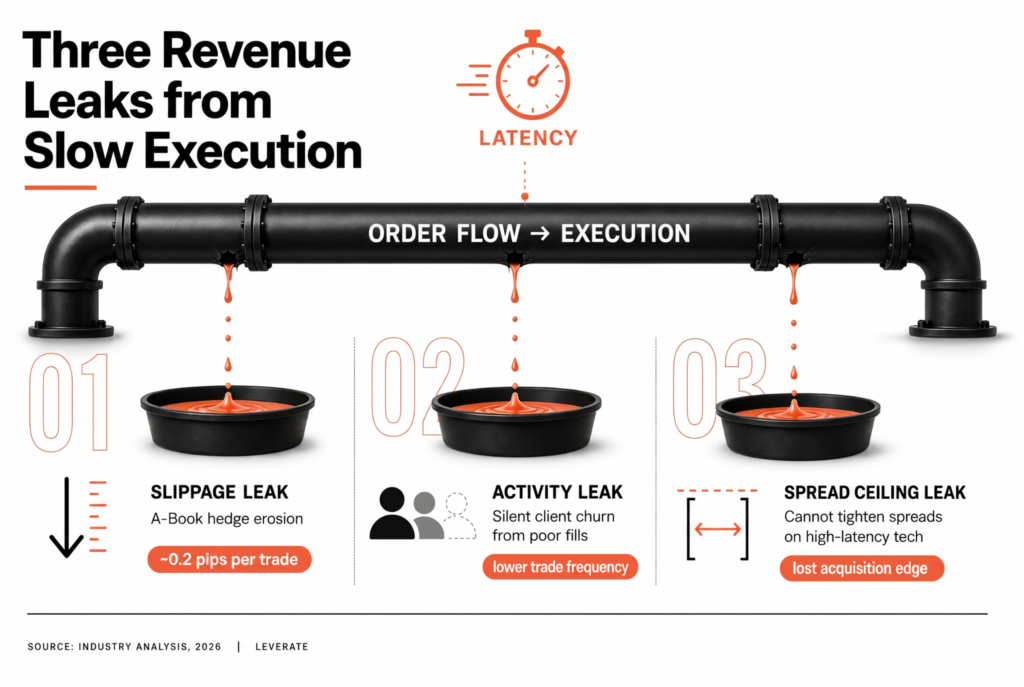

Execution speed impacts broker revenue through three primary channels. The first is slippage cost: when a trade executes at a price different from the requested price, the broker may absorb that difference depending on the book model. For A-book brokers, slippage that occurs in the liquidity provider leg of the trade can erode the spread margin captured on the client side. For B-book or hybrid brokers, slippage on hedge trades directly affects the cost of managing retained exposure.

The second channel is client behaviour. Traders who experience consistent execution delays or poor fill quality tend to reduce their trading frequency or migrate to other platforms. This effect is not always captured in standard churn metrics because the client account may remain open while activitygradually decreases. Among active, high-frequency traders, fill quality is one of the most closely monitored metrics, and sustained underperformance leads to disengagement faster than many brokers anticipate.

The third channel is the broker’s ability to offer competitive spreads. A platform with consistently fast and accurate execution may offer narrower spreads on high-volume instruments without the fill quality risk that would arise on a platform with higher latency. This matters for client acquisition in segments where traders actively compare spread quality across platforms before making a deposit.

What Is Slippage in Trading?

Slippage is the difference between the price at which a trade was requested and the price at which it was executed. It occurs when the market price moves between the moment the order is submitted and the moment it reaches the execution venue. In fast-moving markets, even a delay of 10 to 20 milliseconds can produce measurable slippage on large-notional trades.

Slippage can be positive or negative from the client’s perspective. Positive slippage occurs when the execution price is better than the requested price, which happens when the market moves favourably in the interval between order submission and execution. Negative slippage, which is more commonly discussed, occurs when the execution price is worse than requested. For the broker, the direction of slippage affects the cost of managing the book differently depending on the operating model.

In practical terms, slippage is most pronounced during three conditions: high-volatility market events such as central bank announcements or major economic data releases; periods of low liquidity such as early-morning or end-of-day sessions in certain instruments; and in infrastructure environments where the execution path involves multiple hops or legacy components that add processing time at each step.

How Does Slippage Affect Broker Profitability?

The direct cost of slippage to a broker depends on how the book is structured and how the platform handles partial fills and re-quotes. An A-book broker that consistently achieves better-than-requested execution passes most of the benefit to the client, supporting fill quality metrics, but does not directly improve the broker’s margin. Where slippage becomes a direct cost is in the hedge leg: if the broker covers its B-book exposure with a liquidity provider and the hedge executes with negative slippage, the cost of that difference comes off the broker’s book.

At scale, even small average slippage figures compound significantly. A broker processing 10,000 A-book trades per day with an average negative slippage of 0.2 pips on forex pairs is absorbing a cost that, depending on notional volumes, can represent a meaningful reduction in daily operating margin. The same calculation applies to the cost of re-quoting, where trades are rejected and resubmitted because the quoted price was no longer available at the time of execution.

According to a 2026 report on retail trading infrastructure reviewed by FX News Group, brokers operating on outdated execution infrastructure report higher average slippage rates and elevated re-quote frequencies compared to those running on current-generation platforms, with the cost gap widening during high-volatility market events.

Source: FX News Group, 2026

| Execution Issue | Direct Cost Impact | Indirect Revenue Risk |

| Negative slippage on hedge | Direct deduction from margin | Low |

| Re-quotes on client fills | Processing overhead | High: client churn risk |

| Delayed stop-out execution | Negative balance exposure | Medium: compliance risk |

| LP response latency | Wider effective spreads | Medium: reduced competitiveness |

What Causes Delays in Trade Execution?

Execution delays originate from multiple points in the trade lifecycle, and identifying which component is generating the latency requires systematic measurement rather than assumption. The most common sources of delay fall into three categories: network latency between the trading platform and the execution server, processing latency within the broker’s own systems, and liquidity provider response time.

Network latency is a function of physical distance and network architecture. A trading platform hosted in a data centre that is geographically distant from the broker’s liquidity providers introduces unavoidable round-trip delays that compound at high order volumes. Co-location, where the broker’s execution infrastructure is hosted in the same data centre as the primary liquidity provider, is the most direct mitigation for this category of latency.

Processing latency within the broker’s own systems is often generated by legacy components, order management systems that were not designed for current-generation trading volumes, or integration layers between the trading platform and back-office systems that add processing steps to the execution path. These delays are typically more addressable than network latency because they are within the broker’s control, but they require a technical audit to identify accurately.

Liquidity provider response time is the external component that brokers can influence through provider selection and aggregation architecture. Using a single liquidity provider with no failover creates a dependency that becomes a latency risk during periods of high market activity. Aggregating multiple providers and routing orders based on real-time price and fill quality metrics can reduce this risk, though the aggregation layer itself introduces additional processing latency overhead that must be accounted for.

How Do Brokers Improve Execution Performance?

Improving execution performance typically requires action at the infrastructure, configuration, and monitoring levels simultaneously. Infrastructure improvements address the underlying latency sources: co-location, network path optimisation, and upgrading legacy components. Configuration improvements address how the trading platform manages orders, including fill-or-kill versus fill-at-best settings, partial fill handling rules, and the parameters used for re-quote decisions. Monitoring improvements is what makes the other two sustainable: without consistent measurement of execution quality across instruments, trading sessions, and client segments, it is not possible to identify where degradation is occurring or whether improvements have had the intended effect.

Leverate’s premium trading platform is designed with execution performance as a core operational requirement. The platform infrastructure supports co-location deployment, connects to Leverate Prime Liquidity with configurable aggregation, and provides execution quality reporting through the Broker Portal. For brokers where execution speed impacts broker revenue in ways that current infrastructure cannot adequately address, the Leverate MT4/5 solutions ecosystem provides a technical foundation for improvement.

Frequently Asked Questions

How does execution speed impact broker revenue?

Execution speed impacts broker revenue through three main channels: slippage costs on hedge trades, client behaviour changes driven by poor fill quality, and constraints on the broker’s ability to offer competitive spreads. The cumulative effect of execution delays is often underestimated because individual events appear minor, but across high volumes over time, the combined cost can represent a meaningful reduction in operating margin.

What is slippage in trading?

Slippage is the difference between the price at which a trade was requested and the price at which it actually executed. It occurs when the market price moves between order submission and execution, which can happen in fractions of a second during volatile conditions. Slippage can be positive or negative; positive slippage benefits the trader while negative slippage results in a worse-than-requested fill. The cost implications for brokers depend on the book model and where in the execution path the slippage occurs.

How does slippage affect broker profitability?

Slippage affects broker profitability most directly when it occurs in the hedge leg of A-book or hybrid-model trades. If the broker executes a client order at one price but the corresponding hedge fills at a worse price, the difference is a direct cost to the broker. At scale, even average slippage of a fraction of a pip per trade can accumulate into a meaningful daily cost. Slippage also affects profitability indirectly through its impact on client retention.

What causes delays in trade execution?

Execution delays are caused by network latency between the trading platform and execution servers, processing latency within the broker’s own order management and integration systems, and liquidity provider response time. Each source requires a different mitigation: co-location for network latency, system audits and upgrades for processing latency, and provider aggregation for LP response time. In practice, multiple sources contribute simultaneously and benefit from a coordinated infrastructure review.

How do brokers improve execution performance?

Brokers improve execution performance by addressing the infrastructure layer through co-location and network optimisation, the configuration layer through order handling settings and re-quote rules, and the monitoring layer through consistent measurement of execution quality by instrument and session. Improvement initiatives that address only one layer without the others tend to produce limited results. Platforms designed with execution performance as a foundational requirement reduce the overhead of these improvements considerably.

What is the relationship between latency and broker spread competitiveness?

Brokers with lower execution latency can typically offer tighter spreads on high-volume instruments without the fill quality risks that would arise on a slower platform. When a broker quotes a tight spread, the fill quality at that spread depends on the platform’s ability to execute before the market price moves enough to make the quoted price undeliverable. Higher latency increases the frequency of fills at worse prices, which either erodes the broker’s margin or results in re-quotes that create friction for clients.

Does execution speed matter more for certain client segments?

High-frequency traders and algo traders are significantly more sensitive to execution latency than casual retail traders because their strategies often depend on precise fill prices. For these segments, even small execution quality differences can determine whether their approach remains viable on a given platform. Brokers targeting professional or high-volume trader segments need to prioritise execution performance as a core product attribute. Brokers focused on entry-level retail traders may find that other factors, such as educational content and user experience, are more influential in retention.

How can brokers measure their current execution quality?

Execution quality is typically measured through fill rate (the percentage of orders filled at or better than the requested price), average slippage per instrument and session, re-quote frequency, and order-to-fill latency measured in milliseconds. These metrics should be tracked over time and segmented by instrument class, trading session, and client type to identify patterns. The Broker Portal within Leverate’s ecosystem provides reporting tools that support this kind of execution quality monitoring on an ongoing basis.

Disclaimer:

This content is based on multiple sources and is provided for educational purposes only. It does not constitute financial, legal, or investment advice.